How to Start Investing With $100 (Or Less)

TL;DR

You really can start investing with $100. Or $50. Or $5. Fractional shares have removed the "I need to buy a whole share" problem [1].

$100 a month at 6.8% real return for 40 years works out to about $248,000 in today's dollars [2][3].

The right place for your first $100 depends on whether you have a 401(k) match available and whether your income qualifies for a Roth IRA [4][5].

Avoid micro-investing apps that charge a flat monthly fee. On a $100 balance, $1/month is a 12% annual fee [6].

A single low-cost total stock market ETF in a Roth IRA at Fidelity, Schwab, or Vanguard is a perfectly reasonable place to start [7][8][9].

The "I Don't Have Enough to Start" Myth

The most common reason people give me for not investing is some version of "I don't have enough money yet." For most of them, the number they're chasing is somewhere between $1,000 and $5,000. Until they have that, the thinking goes, it isn't worth bothering.

That logic was actually true in 1995. It hasn't been true since fractional shares became broadly available at major brokerages around 2019 and 2020 [1]. A fractional share is exactly what it sounds like. If a share of an ETF is $250 and you have $25, you can own 0.10 shares. The dividend gets paid proportionally. The growth gets paid proportionally. Owning 0.10 shares versus 10 shares is the same investment at a different size.

Fidelity, Schwab, Vanguard, and most major custodians now support fractional share purchases [7][8][9]. The minimum to open and fund a Roth IRA at any of them is $0.

The "I don't have enough" excuse has expired. As a CERTIFIED FINANCIAL PLANNER® (CFP®) professional working with people across a wide range of income levels, I'd argue the bigger problem now is that small starts get dismissed before they get started.

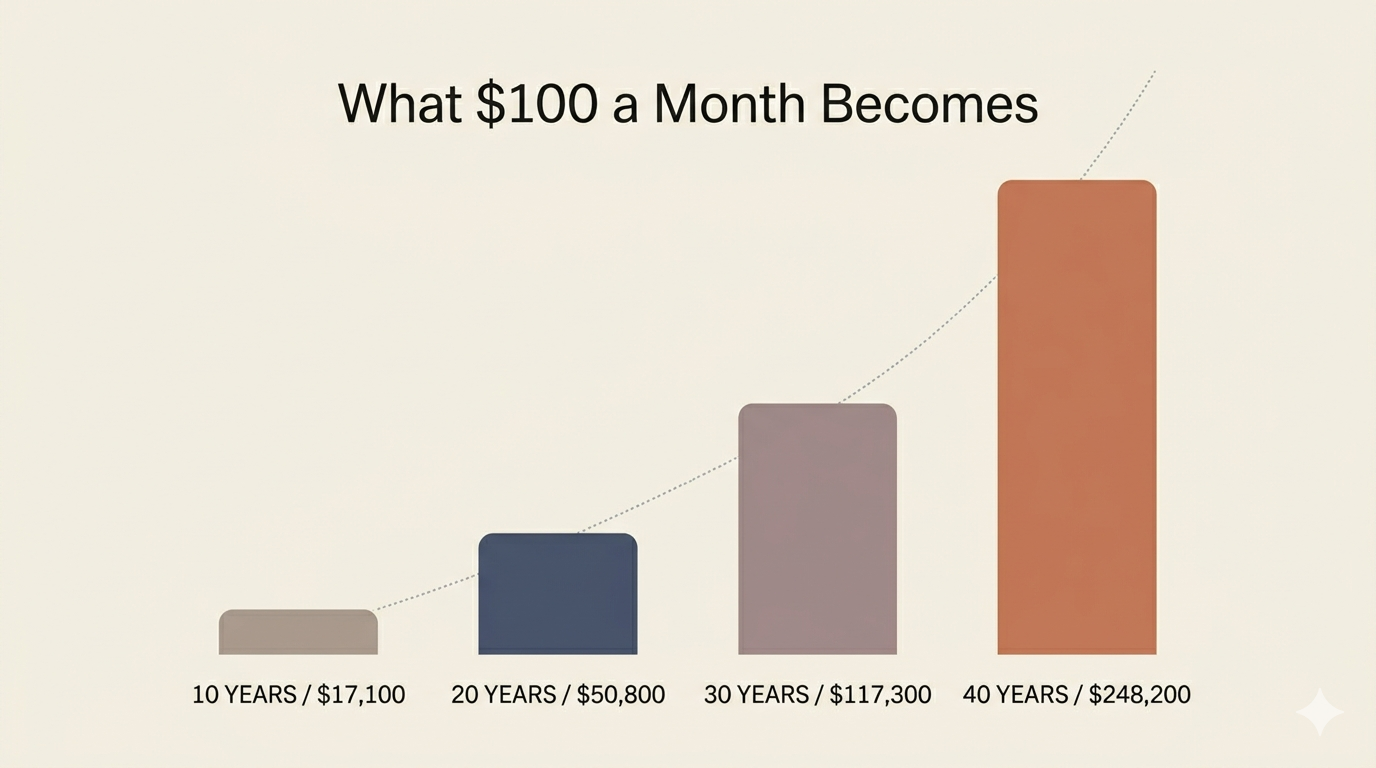

What $100 a Month Actually Becomes

Using the Fisher equation to convert the S&P 500's roughly 10% nominal historical return to a real, inflation-adjusted return of about 6.8% [2][3] (full math in The Complete Guide to Investing for Beginners), here's what $100 a month grows to, compounded monthly:

After 10 years: about $17,100

After 20 years: about $50,800

After 30 years: about $117,300

After 40 years: about $248,200

Hypothetical only. Past performance does not guarantee future results. Assumes $100 monthly contributions at a 6.8% real annual return, compounded monthly, all values in today's dollars.

Hypothetical only. Past performance does not guarantee future results.

A quarter of a million dollars from $100 a month, after inflation. The most important variable in those numbers is the number of years, not the contribution size. Starting at 25 with $100/month for 40 years produces more wealth than starting at 35 with $250/month for 30 years.

Where to Actually Put Your First $100

The order matters more than most beginners realize.

If you have a 401(k) match, that's where the first dollar goes. A typical employer match is 50 cents on the dollar up to 6% of salary [4]. If you're earning $50,000, that's a $1,500-per-year match for contributing $3,000. Walking past it is the most expensive mistake in personal finance.

If your 401(k) doesn't have a match (or you don't have a 401(k) at all), open a Roth IRA at Fidelity, Schwab, or Vanguard [11]. The 2026 contribution limit is $7,500 [5]. Income phase-outs apply, but at $100/month most early-career earners are well under any limit.

Once that's open, buy a single diversified, low-expense-ratio total U.S. stock market ETF. The Vanguard Total Stock Market ETF (VTI) has an expense ratio of 0.03% [10]. Schwab and Fidelity have comparable products [13][14]. Set up an automatic monthly contribution of $100. Let it run.

Three steps. Maybe 30 minutes of work, mostly waiting on the bank link to verify.

What to Avoid

A few traps catch beginners with small balances disproportionately.

Apps with flat monthly fees. Some popular micro-investing apps charge $1 to $5 per month for a "subscription." On a $100 balance, $1/month is a 12% annual fee. On a $500 balance, $1/month is 2.4%. Those fees only stop being abusive once your balance is several thousand dollars [6]. A standard brokerage account at Fidelity, Schwab, or Vanguard charges $0 for the same basic functionality.

Picking individual stocks. With $100, you don't have enough to be diversified across individual companies, and concentrating it in one or two turns an investment into a gamble. A total market ETF gives you exposure to roughly 3,500 U.S. companies in a single trade [10].

What to Do This Week

Three things, in order:

Confirm your 401(k) match if you have one. If you're not getting it, increase your contribution rate today.

Open a Roth IRA at Fidelity, Schwab, or Vanguard. Link your bank account.

Set up an automatic $100/month transfer into a single total-market ETF. Pick one of VTI, SCHB, or FZROX. The differences between them at this level are small enough that any of the three is reasonable.

Future you, looking at a six-figure balance built on $100/month contributions, will not remember which one you picked.

Want more posts like this one?Sign up for the Melby Money Newsletter. A couple of emails a month. Plain English, real numbers, no spam.

FAQs

Should I start with $100 or wait until I can do more?

Start with $100. The behavior of investing matters more than the dollar amount in the early years. You can always increase the contribution. You can't get back the time you spent waiting.

Are robo-advisors worth using when I'm starting small?

Maybe. The case for using one is that it picks the funds and rebalances for you. The case against is that the typical 0.25% management fee compounds against you for decades [12]. If a robo gets you off the sidelines and you would not start otherwise, the fee is worth it. If you're willing to do the very basic work of buying one ETF yourself, you'll come out ahead long term.

What if I can only do $25 or $50 a month?

Same playbook, smaller number. The math works the same way. $50/month at the same return assumption grows to about $124,000 over 40 years [15]. Still meaningful.

References

[1] U.S. Securities and Exchange Commission. "Fractional Share Investing." https://www.sec.gov/files/Fractional-Share-Investing.pdf

[2] Macrotrends. "S&P 500 Historical Annual Returns." https://www.macrotrends.net/2526/sp-500-historical-annual-returns

[3] U.S. Bureau of Labor Statistics. "Consumer Price Index Historical Tables." https://www.bls.gov/cpi/

[4] U.S. Department of Labor, Employee Benefits Security Administration. "What You Should Know About Your Retirement Plan." https://www.dol.gov/agencies/ebsa/about-ebsa/our-activities/resource-center/publications/what-you-should-know-about-your-retirement-plan

[5] Internal Revenue Service. "2026 Amounts Relating to Retirement Plans and IRAs." Notice 2025-67. https://www.irs.gov/pub/irs-drop/n-25-67.pdf

[6] FINRA. "Investment Fees and Expenses." https://www.finra.org/investors/insights/investment-fees-and-expenses

[7] Fidelity Investments. "Fractional Shares." https://www.fidelity.com/learning-center/trading-investing/fractional-shares

[8] Charles Schwab. "Schwab Stock Slices." https://www.schwab.com/fractional-shares-stock-slices

[9] Vanguard. "Investment Minimums." https://investor.vanguard.com/investor-resources-education/investment-minimums

[10] Vanguard. "Vanguard Total Stock Market ETF (VTI)." https://investor.vanguard.com/investment-products/etfs/profile/vti

[11] Internal Revenue Service. "Roth IRAs." https://www.irs.gov/retirement-plans/roth-iras

[12] U.S. Securities and Exchange Commission. "Investor Bulletin: Robo-Advisers." https://www.sec.gov/oiea/investor-alerts-bulletins/ib_robo-advisers.html

[13] Charles Schwab. "Schwab U.S. Broad Market ETF (SCHB)." https://www.schwabassetmanagement.com/products/schb

[14] Fidelity Investments. "Fidelity ZERO Total Market Index Fund (FZROX)." https://fundresearch.fidelity.com/mutual-funds/summary/31635T708

[15] Investor.gov (U.S. Securities and Exchange Commission). "Compound Interest Calculator." https://www.investor.gov/financial-tools-calculators/calculators/compound-interest-calculator

[16] Federal Reserve Board. "Survey of Consumer Finances." https://www.federalreserve.gov/econres/scfindex.htm

About The Author

Shaun Melby, CFP® provides fee-only financial planning and investment management services in Nashville, TN through his company Melby Wealth Management. Shaun has over 15 years of experience as a financial advisor in Nashville. Shaun created Melby Money to educate the public about finances.

Full Disclosure: Nothing on this website should ever be considered to be advice, research, or an invitation to buy or sell any securities. Please see the Disclaimer page for a full disclaimer.